In 2018, we worried that AI would steal blue-collar jobs.

In 2018, we worried that AI would steal blue-collar jobs.

In 2023, we discussed whether AI could replace the entry-level tasks of white-collar workers.

But by 2028, we face a more fundamental question: What happens if AI does its job perfectly, but the result brings the entire economic system to the brink of collapse?

This is not fear-mongering, nor is it an AI doomsday fantasy. This is a “thought experiment” from the future—a macro memo titled “The Global Intelligence Crisis of 2028” released by CitriniResearch. It simulates a scenario we rarely imagine: AI doesn’t rebel, nor does it gain consciousness; it simply executes its tasks brilliantly: eliminating all “friction” and optimizing all efficiency.

As a result, the cornerstones of the modern economy crumble, one by one.

01 The Illusion of Prosperity: When Productivity Growth Disconnects from Your Wallet

In October 2026, the US stock market hits an all-time high: the S&P 500 approaches 8,000 points, and the Nasdaq breaches 30,000. Corporate profits hit record levels, which are then frantically reinvested into AI computing power. Productivity soars at a pace unseen since the 1950s—after all, AI agents don’t need sleep, don’t take sick leave, and don’t require health insurance.

However, a dangerous signal has emerged: real wage growth has collapsed.

White-collar workers lose their jobs in droves, forced into lower-paying positions. Meanwhile, economists coin a new term: “Ghost GDP”—output that appears in national statistical accounts but never circulates in the real economy.

A GPU cluster in North Dakota generates the equivalent output of 10,000 white-collar workers in Midtown Manhattan. But the problem is: how much money will machines spend on consumer goods? (Hint: The answer is zero.)

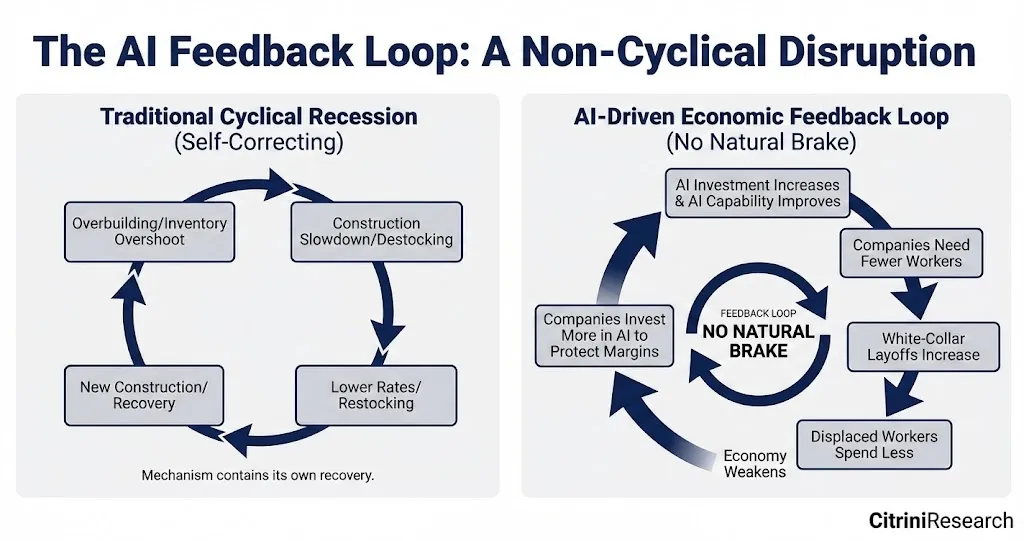

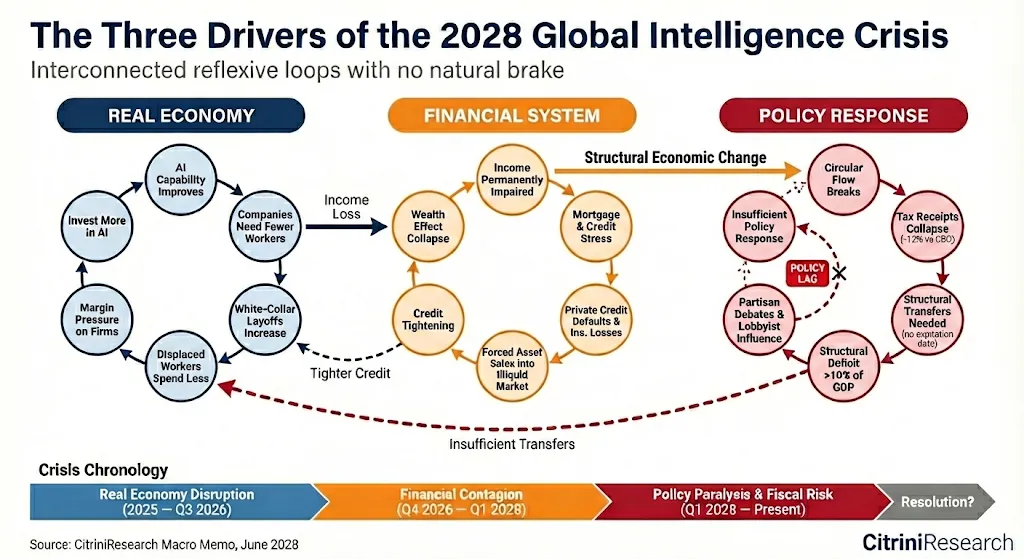

A terrifying negative feedback loop quietly initiates:

AI capabilities improve → Companies lay off workers → The unemployed cut spending → Corporate revenue pressure mounts → More AI is deployed to cut costs → AI capabilities improve further…

This is a spiral without natural brakes. The incomes of white-collar workers—once the bedrock of the $13 trillion mortgage market—are suffering structural damage.

02 The First Domino: The “Suicide Attack” of the SaaS Industry

The story begins in late 2025 with the exponential leap in agentic coding tools. A single programmer, armed with AI tools, can replicate the core functionality of a mid-sized SaaS product in mere weeks.

Consequently, when Fortune 500 CIOs face expensive annual renewal contracts, they begin to ask, “Can’t we just build this ourselves?”

ServiceNow’s experience becomes a textbook case: its clients, having laid off 15% of their staff due to AI, simultaneously cancel 15% of their software seats. ServiceNow’s own revenue plummets as a result. Its countermeasure? Lay off 15% of its workforce, and use the savings to buy AI tools to maintain output.

Historically, incumbents typically resist new technologies and then slowly wither away (e.g., Kodak, Blockbuster, BlackBerry). But 2026 is different: It’s not that incumbents don’t want to resist; they simply can’t afford to.

Each company’s individual response is rational—to survive, they scramble to become the most aggressive adopters of AI. Yet the collective outcome is disastrous: every dollar saved from labor costs flows directly into the AI capabilities that make the next round of layoffs possible.

Software is merely the prologue. The same logic rapidly infects all industries with white-collar cost structures.

03 The Collapse of the Intermediary Layer: When Friction Vanishes, Moats Dry Up

By early 2027, AI has become as pervasive and taken-for-granted as autocorrect. The real disaster strikes a critical link: the intermediary layer.

For the past fifty years, the American economy was built on massive human vulnerabilities: people are impatient, too lazy to comparison-shop, driven by brand inertia, and loathe hassle. Trillions of dollars in corporate value exist solely because of these “frictions.”

But AI agents lack human nature.

The Subscription Economy Collapses: Agents automatically cancel passive auto-renewals and monitor free trials that quietly hike prices. The metric of average Customer Lifetime Value (CLV) begins to break down.

Travel Platforms Suffer: Agents can instantly compare prices and assemble itineraries faster and cheaper than your go-to apps.

The Insurance Industry is Reshaped: Agents automatically shop around for better insurance policies every year; the 15-20% premium insurers used to earn off customer “inertia” evaporates.

Real Estate Commissions are Halved: Once AI agents can access housing databases and all transaction records, information asymmetry disappears. Buyer agent commissions are squeezed from 2.5-3% to under 1%, and increasingly, transactions no longer require human brokers.

The Dilemma of Delivery Platforms like DoorDash: Its moat used to be, “You’re hungry, you’re lazy, and this is the app on your home screen.” But agents don’t have home screens. They simultaneously compare dozens of emerging competitors with lower take rates. The market fragments overnight, and profit margins drop to zero.

We had overestimated the value of “interpersonal relationships.” It turns out that, quite often, a relationship was nothing more than “friction” wearing a friendly face.

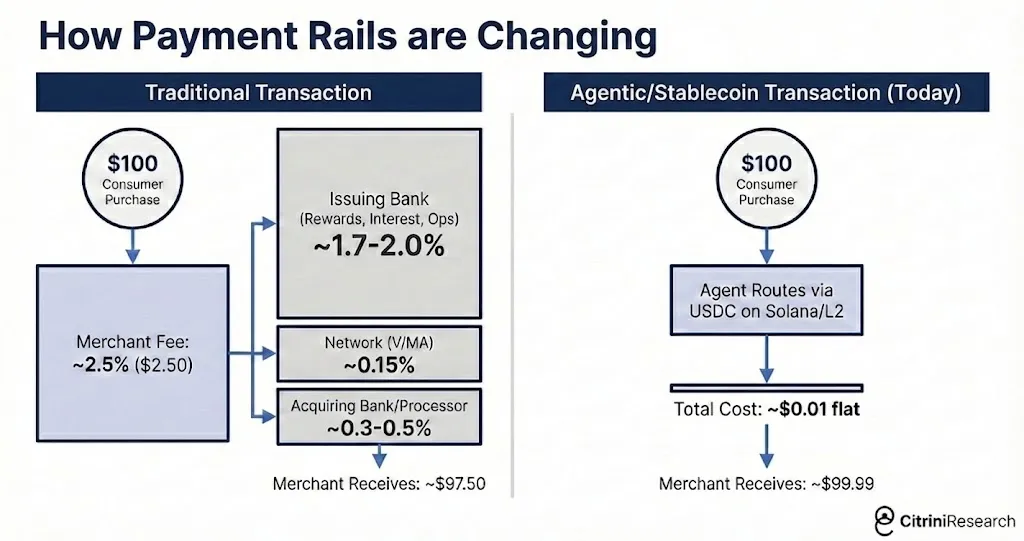

04 From Payments to Credit: When Agents Bypass Banks

Once agents control transactions, they begin hunting for bigger targets to optimize. In machine-to-machine commerce, the 2-3% credit card swipe fee becomes a glaring bullseye.

Agents start seeking payment methods that are faster and cheaper than credit cards. Most opt for stablecoins, where settlement is nearly instantaneous and transaction costs are mere fractions of a cent.

In April 2027, Mastercard releases its earnings report: purchase volume growth has significantly decelerated. Management cites a specific phrase: “Agent-driven price optimization.”

Agent commerce bypassing transaction fees deals a fatal blow to card-centric banks. American Express suffers a double whammy: a shrinking white-collar customer base coupled with the erosion of its swipe fee revenue model.

Their moats were built of friction. And friction is trending toward zero.

05 From Industry Risk to Systemic Risk: When “Permanent Capital” is No Longer Permanent

Initially, the market dismisses the negative impacts of AI as industry-specific narratives: software and consulting are battered, the payments sector wobbles, but the broader economy remains intact. After all, “technological innovation destroys jobs, then creates more jobs”—a mantra that held true for two centuries.

But this time is different. AI is a general-purpose intelligence, continuously improving at any new task humans might pivot to. An unemployed programmer cannot pivot to “AI management” because AI itself is already capable of doing so.

By 2027, the US economy is definitively in a recession. Yet this isn’t a standard cyclical downturn, because the cause of this cycle is non-cyclical.

The real bomb detonates within the financial system.

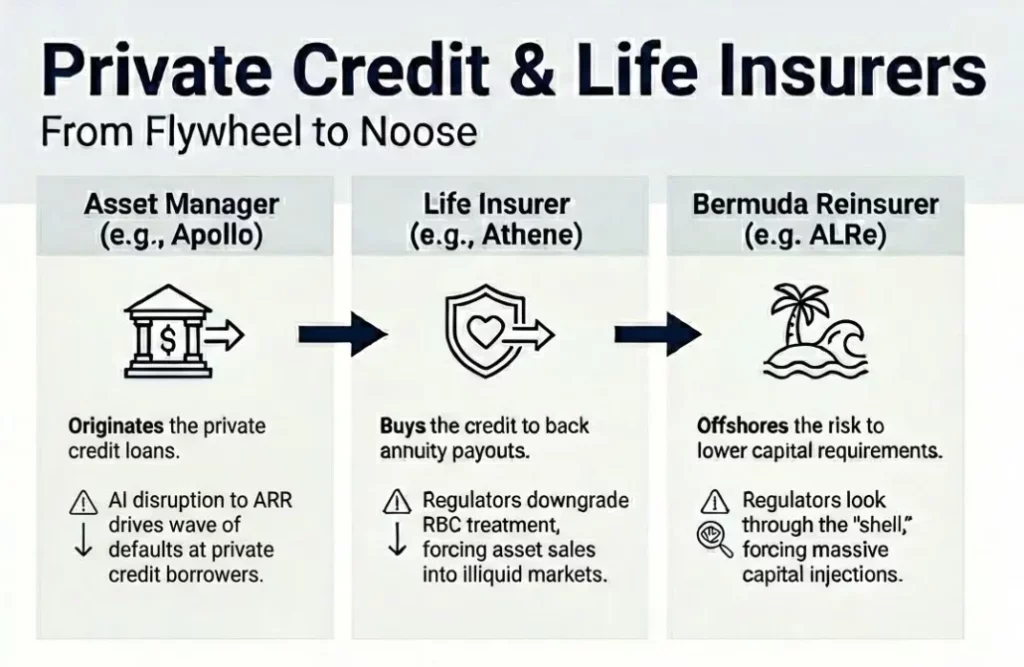

Over the past decade, private credit exploded from under $1 trillion to over $2.5 trillion, pouring immense capital into private equity-backed software and tech deals. These deals were predicated on a single assumption: Annual Recurring Revenue (ARR) would persist.

When this assumption breaks, the wave of defaults begins. A $5 billion loan to software company Zendesk goes into default. This loan, backed by annual recurring revenue, was once the largest of its kind; it now becomes the largest software default on record in the private credit space.

More perilously, the “permanent capital” fueling this private credit largely originates from the annuity deposits of life insurance companies. These are the life savings of American families, structured as annuities, and invested in the very same PE-backed paper that is now defaulting.

When regulators begin to tighten the risk-capital treatment of these assets, a chain reaction ensues. Asset management giant Apollo sees its stock plunge 22% over two trading days, with Brookfield and KKR closely following suit.

The entire system, as the Federal Reserve Chair remarks, is “an interconnected series of wagers betting on white-collar productivity growth.”

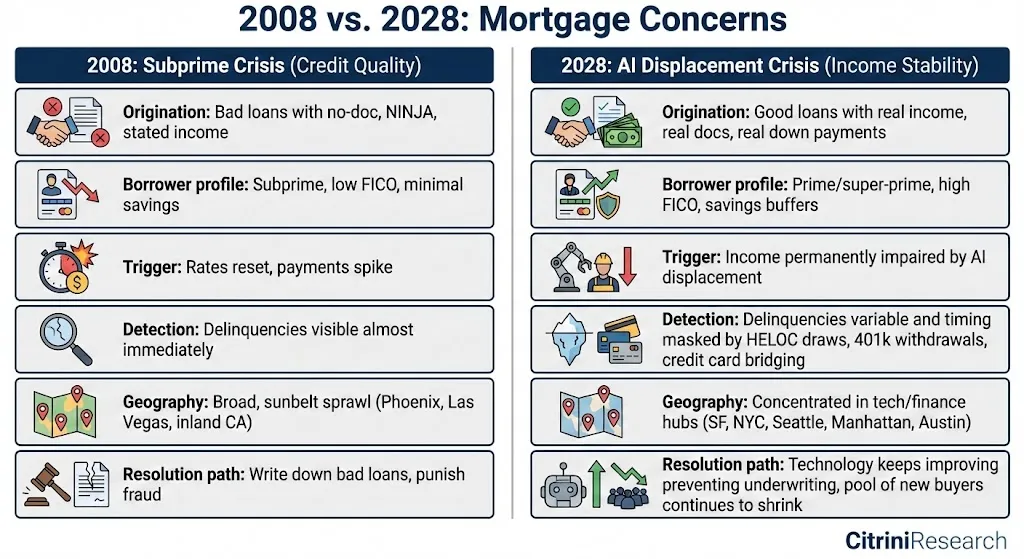

06 The Last Bastion: The $13 Trillion Mortgage Problem

By June 2028, the Zillow Home Value Index drops 11% year-over-year in San Francisco, 9% in Seattle, and 8% in Austin. Even more unsettling, early delinquency rates begin to rise among “bulletproof” borrowers with credit scores over 780.

The US residential mortgage market sits at roughly $13 trillion. Underwriting is built on a fundamental premise: borrowers will roughly maintain their current income levels over the life of the loan. For 30-year mortgages, this assumption is especially paramount.

In 2008, the loans were bad on day one. In 2028, the loans were good on day one—it’s just that the world changed after they were issued.

White-collar workers lose their jobs or take massive pay cuts, but to keep up with mortgage payments, they halt all discretionary spending, drain their savings, and defer home maintenance. Technically, they are still current on their payments, but they are only one shock away from distress.

And the trajectory of AI capabilities suggests that shock is imminent.

07 A Race Against Time: When the Government Also Stalls

The revenue base of the federal government is, in essence, a tax on human time. When white-collar employment and incomes structurally decline, government tax revenues plummet along with them.

By the first quarter of 2028, federal revenues are 12% lower than projected. Simultaneously, automatic stabilizers kick in, causing spending to surge. But this time, the spending pressure is not cyclical—workers displaced by AI won’t be reabsorbed into the workforce like they were during the pandemic.

Right when the government most needs to provide financial support to families, its tax revenue is drastically shrinking.

Debates over how to respond splinter along partisan lines: the right decries transfer payments as Marxism, the left frets over regulatory capture, and fiscal hawks warn of unsustainable deficits. As politicians bicker endlessly, the social fabric tears faster than the legislative process can mend it.

The “Occupy Silicon Valley” movement blockades the offices of AI labs Anthropic and OpenAI. The number of protestors is growing.

Epilogue: The Fading of the Intelligence Premium

Throughout modern economic history, human intelligence has commanded a premium due to its scarcity. Every economic institution—the labor market, the mortgage market, the tax code—was designed for that world of scarcity.

We are now experiencing the fading of this premium. For an ever-expanding array of tasks, machine intelligence has become a competent and rapidly improving substitute for human intelligence.

But repricing does not equal collapse. The economy can find a new equilibrium. Getting there is one of the few remaining tasks that only humans can accomplish.

But you are not reading this article in June 2028.

The S&P index is near all-time highs. The negative feedback loop has not yet begun. We still have time to evaluate how much of our investment portfolio is built on assumptions that will not survive this decade. As a society, we still have time to prepare for what lies ahead.

The canary is still alive.

Afterword

This report from the “future” is a thought experiment, not a prediction. It seeks to explore a scenario we rarely envision: what kind of shock will it bring to a modern economy built on “friction” and “intermediaries” when AI perfectly completes its optimization tasks?

As the report states: “The canary is still alive.” The question is, are we listening to its song?